Thanks to bitcoin, blockchain is the buzzword on everyone’s lips right now. Many people see it as something that enables cryptocurrencies, but it is much more than that. At its core, it is a technology that can be the backbone of the new decentralized web 3.0 revolution unfolding in front of us. The developments in this space are evolving rapidly, and it’s impossible to talk about it all. So for this article, we will focus on how blockchain works, its key components, characteristics, and applications.

History

Many people have called blockchain the next big thing after the internet, and rightly so. Though the concept of blockchain is quite new, its fundamentals are not. Back in 1983, American cryptographer David Chaum came up with the idea of using cryptography in finance. His works resulted in something called the blind signature protocol. Its design disguises the identity of the people involved in a transaction without compromising on safety and reliability. The protocol can prove the authenticity of a transaction without revealing any personal information. It is often considered the first attempt in creating something similar to the current blockchain technology.

How blockchain works

Blockchain is a combination of cryptography and distributed computing. It is a chain of blocks connected in a linear and chronological order. Each block is a stack of information uniquely identified by a hash value which is the product of a cryptographic protocol that encrypts the data. The hash of each block is also linked to the previous block’s hash, forming a chain that helps keep track of the chronology of the entire data.

In addition to encryption, the data also needs to be validated before adding to the blockchain. For this, the processing node checks with the other nodes in the network whether the data is feasible or not. If the majority of nodes accept the data, it is considered valid. The information is then encrypted and added to the blockchain. Finally, this newly updated data is broadcasted to every node for bookkeeping.

Key Characteristics

Decentralization

Before exploring decentralization, we need to understand why centralized infrastructure is not ideal. With a centralized database, we place all our trust in one entity to add and store data. In a decentralized system, the information is no longer controlled and managed by a single organization. Therefore, it reduces the risk of any potential data mismanagement and also removes the element of trust because protocols govern everything.

Cryptography

Cryptography is nothing but a set of algorithms that masks the underlying data. It will protect the data from being manipulated by hackers or other adversaries. Every block of data added to the blockchain is encrypted. The encryption produces a 64-bit hash value representing the data in the block and the previous block’s hash. This way, each block is connected to the previous one. If someone manages to tamper with the data, the block’s hash would change, which would trigger a chain reaction and make all the blocks invalid.

Immutability

One of the critical aspects of blockchain is its data immutability. Blockchain is governed by a set of highly sophisticated rules which are unlikely to be breached. In order to add data to the network, its validity must be confirmed by more than 50% of the nodes. If the majority of the nodes reject the data, then the data will be considered invalid and is not added to the block. Unlike centralized systems, the criminals manipulating the data need to do so on multiple nodes in a network to be successful, which is very hard.

Blockchain Applications

Decentralized Storage of Information

Blockchain is a network of distributed ledgers. As a result, it is the most secure and reliable way of storing data with little worry of it getting manipulated. It makes blockchain a desirable place to keep important records or any transactions.

One way to use this technology is to create a decentralized database to store the health information of the citizens of a country. Health data is critical and can be corrupted by enemies to destabilize a nation during wartime. Currently, many organizations store such data in centralized databases controlled and managed by themselves. Centralized databases have a single point of failure, making it easy for bad actors to attack the network and tamper with the information. A blockchain network would make such an act incredibly hard because of cryptography and its decentralized nature.

Smart Contracts

Introduction

Back in 2009, when we first saw blockchain in action in the bitcoin network, it was primarily used for coordinating distributed ledgers. But a more significant improvement came in 2013 when Vitalik Butrin first released his paper where he proposed to use blockchain technology to execute smart contracts. Later in 2015, his ideas took the shape of the Ethereum network.

How smart contracts work

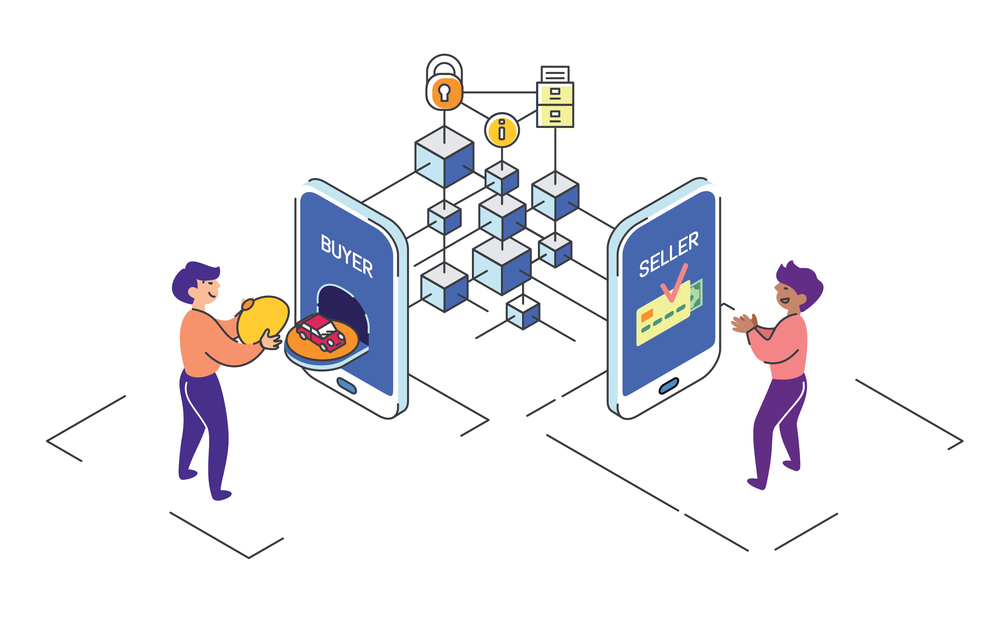

Smart contracts are the digital version of regular contracts. They are just a piece of code stored and executed on the blockchain. Their purpose is to automate transactions without the oversight of a middleman, thus increasing speed and reducing transaction costs. The terms of a smart contract are embedded into the computer code. This code then runs to fulfill the contract accordingly.

Use case

For example, Amazon acts as a mediator between the buyer and seller on its platform. Whenever you buy something on Amazon, you pay them the money and trust Amazon to deliver it to the seller or return your money if the product doesn’t arrive. This entire process can be automated by putting all the conditions into a piece of computer code running on the blockchain.

Token Economies

Introduction

The next step for blockchain is to go from automating certain transactions through smart contracts to automating the coordination of human behavior without the need for a central organization to oversee it. Token economies are a way to do that. A token economy aims to incentivize positive human behavior with tokens that can then be redeemed for a reward. It’s not a new concept, but with blockchain, you can achieve this very same thing in a much bigger and more automated way. To understand how token economies work, we need first to understand what a token is and how it is different from our existing currencies like the US dollar.

what are tokens?

Tokens are quantifiable units of value that can be programmed to adhere to a network’s rules. They can be any form of value, both tangible and intangible. For instance, the number of social media followers or number of kills in the game of PUGB could have some intangible value that can be exchanged for tokens and not something like US dollars. The current fiat currencies are limited in this sense. These unique characteristics of a token give token economies the power to incentivize or punish human behavior like never before.

Use case

Let’s look at a token economy example. We could create something called an air token that is given out for doing environmentally friendly things, like planting trees. Then make every act of deforestation pay the price in these air tokens. So, the demand for these tokens would increase whenever deforestation increases, incentivizing people to be more environmentally friendly. Automated market systems based on blockchain technology would control the value of this token. The people participating in this economy could save the air token they earned or could exchange these tokens for something else as tokens are fungible.